Australia

Australia USA

USA UK

UK Ireland

Ireland

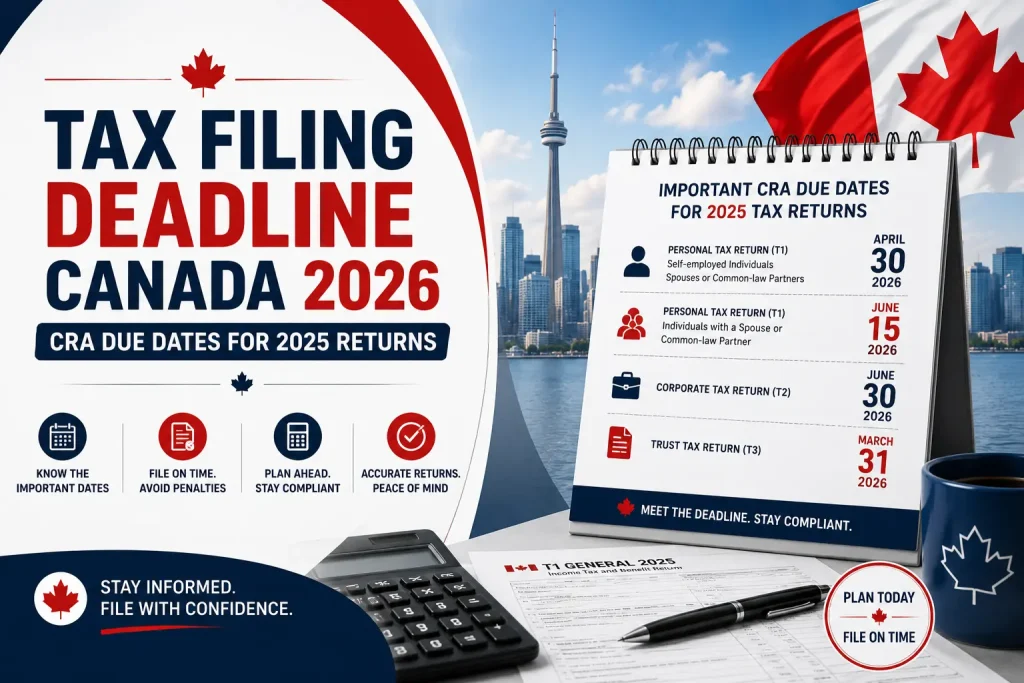

CRA Tax Filing Deadlines for 2026 at a Glance

This table is the scannable reference worth bookmarking. All dates apply to the 2025 tax year.

| Taxpayer/Return Type | 2026 Deadline | Notes |

| Individuals (employees, pensioners) — T1 | April 30, 2026 | Balance owing also due April 30 |

| Self-employed individuals — T1 | June 15, 2026 | Balance owing still due April 30, 2026 |

| Spouse/common-law of self-employed — T1 | June 15, 2026 | The same extended deadline applies |

| Corporations — T2 | 6 months after fiscal year-end | E.g., Dec 31 year-end → June 30, 2026 |

| Trusts and Estates — T3 | 90 days after trust year-end | March 31, 2026, for Dec 31 year-ends |

| GST/HST Annual Return | 3 months after fiscal year-end | Varies by reporting period |

| T4 / T4A Slips (employer) | March 2, 2026 | Normally, Feb 28 moves to the next business day in 2026 |

| RRSP Contribution Deadline | March 2, 2026 | For a 2025 tax year deduction |

All deadlines are based on current CRA guidance for the 2025 tax year. Always verify current dates at canada.ca/cra before filing.

Understanding CRA Filing Deadlines by Taxpayer Type

- Employees, Salaried Individuals & Pensioners

April 30, 2026, is the deadline for both filing and payment on a standard T1 Tax Return. If April 30 is a weekend or holiday, the CRA extends the deadline to the next business day (April 30, 2026, is a Thursday, so this is not applicable in 2026).

If you have a simple income on your T4S and regular deductions, this is the last day, and there are no exceptions. If even a one-day-late return is filed with a balance owing, the late-filing penalty is applied.

- Self-Employed Individuals and Contractors

The filing deadline is extended to June 15, 2026, but this extension applies only to filing. Until April 30, 2026, any balance due will remain due. This is the only tax filing deadline that is frequently confused in Canada.

If you owe $5,000 and still file on June 1 (which is still within the extension), the CRA will start the daily compound interest on the $5,000 balance, beginning on May 1. The extension of June 15 also affects the spouse or common-law partner of the self-employed person, even if they earn only employment income.

- Corporations Filing T2 Returns

There is no fixed calendar date for T2 tax return filing, unlike personal tax. However, the deadline is always 6 months after the corporation’s fiscal year-end (June 30 for a December 31 year-end, September 30 for a March 31 year-end, and so on).

Most corporations have a much earlier payment date: 2 months after FYE. Qualifying Canadian-Controlled Private Corporations (CCPCs) have a 3-month figure. The December 31 (year-end) corporation has to pay by late February, although the T2 isn’t due until June 30. This filing vs. payment error is among the most costly mistakes organisations can make.

- Trusts and Estates Filing T3 Returns

The T3 tax return is due 90 days after the trust tax year-end (which is typically December 31, 2026, for trusts with a year-end on that date).

The CRA recently made changes to its rules, which now require the filing of many bare trusts and family trusts which previously believed that they did not need to file. If a trust fails to confirm its 2025 filing status, check that it is confirmed by the March 31 deadline.

The Most Common CRA Deadline Mistakes Canadian Businesses Make

- Assuming the self-employed extension covers the balance owing. It does not; payment is still due April 30, even if you file June 15.

- Filing the T2 on time, but paying late. There is a difference between the two filing deadlines: 6 months and the 2–3 month payment deadline. When you pay at the time of filing, months’ worth of interest will accrue.

- Not submitting any application by the T3 deadline. Trusts are frequently governed by a lack of their own tax resources, and the 90-day period is a sneaky one for estate trustees.

- Failure to pay quarterly instalments of the GST/HST. If you are an annual filer of GST/HST, you may fall behind on payments of the mid-year instalments, resulting in GST/HST arrears interest.

- Not filing due to inability to pay. This is the costliest mistake. If you file on time, but none of the late-filing taxes is paid, there is no penalty for late filing, just interest.

Why Missing CRA Deadlines Becomes Expensive Faster Than Most Businesses Expect

How the Late-Filing Penalty Works

The CRA will impose a late filing fee of 5% of the remaining balance, plus an additional 1% per month for each month the return is late (to a maximum of 12 months). Interest is not charged until you file a return more than 6 months late, and an 11% charge is imposed on the unpaid balance.

The penalty is doubled if the CRA has issued a formal demand to file in the prior three years and the taxpayer did not pay on time: 10% and 2% per month up to 20 months.

| A Worked Example Suppose that a corporation is eligible for a $30,000 tax payment and files its T2 four months after the deadline. Late-filing penalty: 5% + 4% (4 months at 1%) = 9% of $30,000 ≈ $2,700 In more recent periods, the approximate CRA-prescribed interest rate is 8-10% per year, compounded daily. Interest on $30,000 for 4 months at roughly 9% annually ≈ $900. The additional cost is around $3,600 on the $30,000 bill. |

CRA-prescribed interest rates change quarterly; these figures are approximate. Confirm the current rate at canada.ca/cra before estimating your own exposure.

The Repeat-Offender Multiplier

If your business has a history of late filing and you are requested to file by the CRA, there may be a total penalty of more than 20% for late filing before interest is calculated.

CRA Deadlines That Businesses Often Forget

- Corporate Tax Instalments

Corporations with tax liabilities exceeding $3,000 are required to pay their taxes by instalment payments throughout the year. When a small business owner goes from a refund to owing a T2, a major surprise is that the annual T2 can be filed, but interest will still accrue on the missed payments.

- GST/HST Remittance Deadlines

GST/HST remittances are tied to your reporting cycle (monthly, quarterly or annual) and are not related to your income tax filing deadline. Those filing quarterly must pay within one month of the end of each quarter, and annual filers must file within three months of the end of the fiscal year.

- T4 and T4A Slips

Employers are required to prepare T4 slips and issue them to employees by the last day of February (which is March 2, 2026, for the 2025 tax year, as February 28, 2026, is a Saturday). For employers with several employees, the penalty continues to accumulate for late filing.

- T3 for Trusts: Including Bare Trusts

New CRA guidance now dictates that numerous bare trusts, in-trust accounts and some holding structures have to submit a T3 where they previously did not. This 90-day deadline applies to all trusts, no matter their size, as long as it is after year-end.

Tax Filing Timelines for Corporations Based on Fiscal Year-End

Corporate deadlines move with your fiscal year-end, not the calendar. Use this table to map your own dates.

| Fiscal Year-End | T2 Filing Deadline | Payment Deadline (CCPC) | Payment Deadline (Other) |

| December 31, 2025 | June 30, 2026 | March 31, 2026 | February 28, 2026 |

| March 31, 2026 | September 30, 2026 | June 30, 2026 | May 31, 2026 |

| June 30, 2026 | December 31, 2026 | September 30, 2026 | August 31, 2026 |

| September 30, 2026 | March 31, 2027 | December 31, 2026 | November 30, 2026 |

CCPC = Canadian-Controlled Private Corporation. Payment deadlines apply to the balance of tax owing after instalments. Confirm your exact dates with an accountant or at canada.ca/cra.

What to Do If You Cannot File on Time

- File Anyway: Even Without Full Payment

The single most important thing you can do if you can’t pay is file on time, regardless. The late-filing penalty only applies to late-filed returns; filing on time with a balance owing generates interest only, not the additional 5%-plus penalty. On a $20,000 balance, that difference can exceed $1,000 in the first month alone.

- Request a Payment Arrangement

The CRA allows taxpayers to set up a payment arrangement if they can’t pay in full by the deadline. Interest continues to accrue, but a formal arrangement prevents escalation to collections. Arrangements can be set up through My Account or by calling the CRA Collections line.

- Taxpayer Relief Provisions

The CRA’s Taxpayer Relief program allows penalties and interest to be waived or cancelled in cases of serious financial hardship, natural disaster, or circumstances beyond the taxpayer’s control. Approval isn’t guaranteed, and a formal request must be filed after the fact; it does not pause interest accrual while under review.

How Canadian Businesses Reduce Tax Filing Risk

- Maintain clean, up-to-date bookkeeping year-round so tax preparation isn’t a scramble in the final weeks.

- Set calendar reminders for every CRA deadline relevant to your taxpayer type — not just April 30.

- Understand the difference between your filing deadline and your payment deadline, especially as a corporation.

- If your fiscal year-end isn’t December 31, map deadlines to your specific dates — generic consumer tax articles don’t apply to you.

- Weigh whether your tax complexity justifies professional preparation — for businesses with payroll, GST/HST, and corporate filings, the cost of a missed deadline usually exceeds the cost of outsourcing.

Why Many CPA Firms and SMBs Outsource Tax Preparation

Tax deadlines aren’t a once-a-year event for most businesses. T4 slips, GST/HST remittances, corporate instalments, and T2 filings all run on different cadences throughout the year.

Missed deadlines are almost always a resource problem, not a knowledge problem — the business owner knew the date was coming but didn’t have the capacity to prepare. Outsourced tax return preparation services provide a dedicated resource that tracks every return type. removes the last-minute scramble and takes the penalty risk off the internal team. For CPA firms, outsourcing T4 tax return and T2 preparation during peak season reduces capacity constraints without adding headcount.

CRA Tax Filing Calendar for 2026

| Date | Deadline | Who It Applies To |

| March 2, 2026 | T4 / T4A slips due to CRA | Employers with employees |

| March 2, 2026 | RRSP contribution deadline | Individuals (2025 deduction) |

| March 31, 2026 | T3 trust return due (Dec 31, year-end) | Trusts and estates |

| April 30, 2026 | T1 personal return + balance owing | Employees, pensioners, salaried individuals |

| April 30, 2026 | Balance owing — self-employed | Self-employed (filing deadline is June 15) |

| June 15, 2026 | T1 filing deadline — self-employed | Self-employed individuals and their spouses |

| June 30, 2026 | T2 corporate return (Dec 31 year-end) | Corporations with a December 31 fiscal year-end |

| Ongoing | GST/HST remittances | All GST/HST registrants (per reporting period) |

| Ongoing | Corporate tax instalments | Corporations owing more than $3,000 in tax |

Frequently Asked Questions

Q1: What Is the CRA Tax Filing Deadline for 2026?

The deadline for filing individual Canadian tax returns for 2025 is April 30, 2026. Self-employed individuals and their spouses get until June 15, 2026, to file, but any balance owing is still due April 30. The T2 is not due on a specific date but rather within 6 months of a corporation’s fiscal year end.

Q2: What Happens If I File Taxes Late in Canada?

CRA will apply an interest charge of 5% on the amount of the unpaid balance plus one per cent for each month the return is late, up to a maximum of 12 months. The double penalty is applied if you’ve missed a payment in the past and a demand for payment has been issued. In addition to the penalty, the CRA also applies daily compound interest to any amounts due and payable which are not paid by the deadline from the day after.

Q3: Do Self-Employed Canadians Get Extra Time?

Yes — self-employed individuals and their spouses did until June 15, 2026, to file their T1s. This is an extended filing date only, and any balance due will be due on April 30, 2026, with interest applied from May 1, as of when the filing.

Q4: When Is T2 Corporate Tax Due?

The T2 return will be due to be filed within 6 months of the corporation’s fiscal year-end. When it’s due earlier – 2 months after the end of the financial year for most corporations and 3 months for qualifying CCPCs. The T2 is due Dec. 31, but the balance is due by late February/March.

Q5: Can the CRA Waive Penalties?

Yes, via the taxpayer relief measures. The CRA will cancel or waive penalties and interest if the taxpayer is in serious financial hardship, sick, affected by a natural disaster or other events out of the taxpayer’s control. They will consider each request on an individual basis and cannot guarantee your request will be approved.

Q6: Are Tax Deadlines Different for Corporations?

Yes. Corporations do not have to pay by April 30 – the date of the personal one. The date of the T2 for the corporations is 6 months after their fiscal year-end, and the date of the payment is 2-3 months after the FY end. For instance, when a corporation is a December 31 year-end corporation, it has until late February or March to pay and doesn’t have to file its T2 until June 30.